WAEC: FINANCIAL ACCOUNTING

Quizzes

-

2014 Financial Accounting WAEC Objective Past Questions

-

2014 Financial Accounting WAEC Theory Past Questions

-

2015 Financial Accounting WAEC Objective Past Questions

-

2015 Financial Accounting WAEC Theory Past Questions

-

2016 Financial Accounting WAEC Objective Past Questions

-

2016 Financial Accounting WAEC Theory Past Questions

-

2017 Financial Accounting WAEC Theory Past Questions

-

2017 Financial Accounting WAEC Objective Past Questions

-

2018 Financial Accounting WAEC Objective Past Questions

-

2018 Financial Accounting WAEC Theory Past Questions

-

2019 Financial Accounting WAEC Objective Past Questions

-

2019 Financial Accounting WAEC Theory Past Questions

-

2020 Financial Accounting WAEC Objective Past Questions

-

2020 Financial Accounting WAEC Theory Past Questions

-

2021 Financial Accounting WAEC Objective Past Questions

-

2021 Financial Accounting WAEC Theory Past Questions

Quiz Summary

0 of 9 Questions completed

Questions:

Information

You have already completed the quiz before. Hence you can not start it again.

Quiz is loading…

You must sign in or sign up to start the quiz.

You must first complete the following:

Results

Results

0 of 9 Questions answered correctly

Your time:

Time has elapsed

You have reached 0 of 0 point(s), (0)

Earned Point(s): 0 of 0, (0)

0 Essay(s) Pending (Possible Point(s): 0)

Categories

- Not categorized 0%

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- Current

- Review

- Answered

- Correct

- Incorrect

-

Question 1 of 9

1. Question

(a) What is a source document?

(b) List six types of source documents

(c) State three users of subsidiary books

-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 2 of 9

2. Question

(a) What is a bank reconciliation statement?

(b) State three reasons for preparing a bank reconciliation statement

(c) Explain the following terms

(i) Unpresented Cheques

(ii) Standing order

(iii) Credit transfer

-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 3 of 9

3. Question

(a) Explain the following terms used in not for profit-making organization

(i) Accumulated fund

(ii) Subscription in arrears

(iii) Receipts and payment account

(iv) Income and expenditure account

(v) Entrance fees

(b) Distinguish between shares and debentures

-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 4 of 9

4. Question

(a) List the four main groups of accounting ratios

(b) Identify the accounting ratio which relates to each of the following statements:

(i) A return of GHc10 net profit for every GHc100 invested

(ii) Goods are held on the average for a period of one month before they are sold

(iii) Trade debtors on the average take a period of 33days to settle their debts

(iv) Trade creditors on the average are paid within 44days for credit purchases

(v) Gross profit of GHc40 is made on every GHc100 of net sales

(vi) Current assets is three times that of current liabilities

(vii) Liquid assets is three times that of current liabilities

(viii) For every GHc100 net turnover, GHc17 is made after deducting operational expenses

(ix) Profit covers interest payment 9 times

-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 5 of 9

5. Question

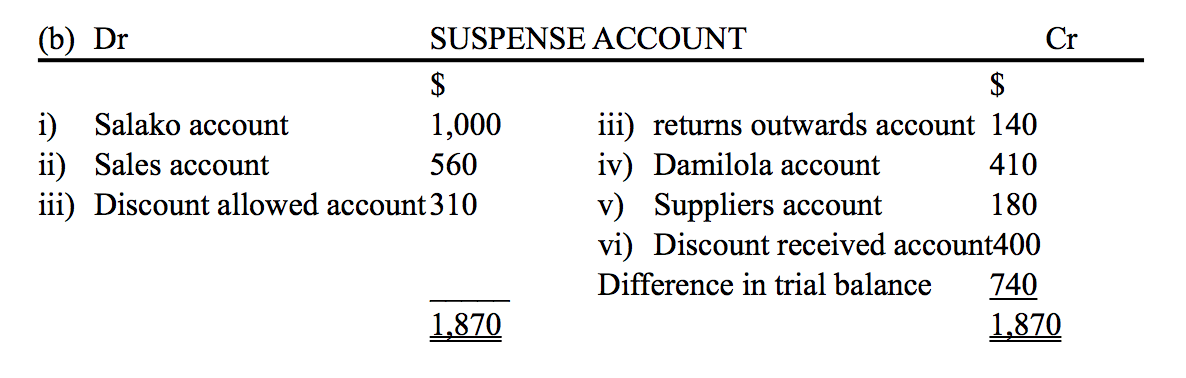

The trial balance of Debra Duwe Enterprises failed to agree. The difference was entered in the suspense account.

The following errors were later detected;

(i) A sum of $1,000 received from Salako has not been posted to his account

(ii) The sales day book was undercast by $560

(iii) Return outwards books was overcast by $140

(iv) Discount received $410 from Damilola had been correctly entered in the cash book but not posted to Damilola’s account

You are required to prepare

(a) Journal entries to correct the errors

(b) Suspense account-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 6 of 9

6. Question

Idayah Limited is a manufacturing company; the following balances were extracted from its records on 31st December 2014

Additional information:

Goods manufactured were transferred to the sales department at cost plus 10%.

You are required to prepare the manufacturing, Trading, Profit, and Loss account for the year ended 31st December 2014-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 7 of 9

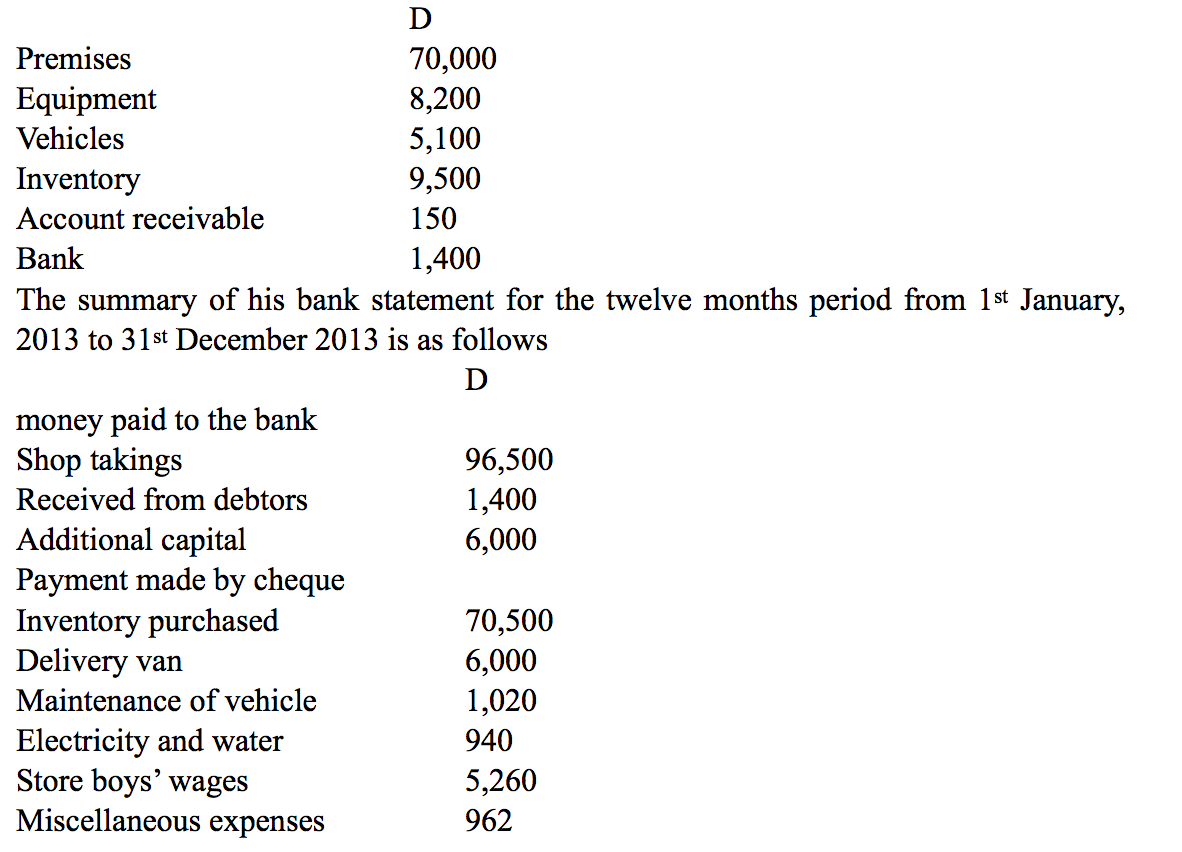

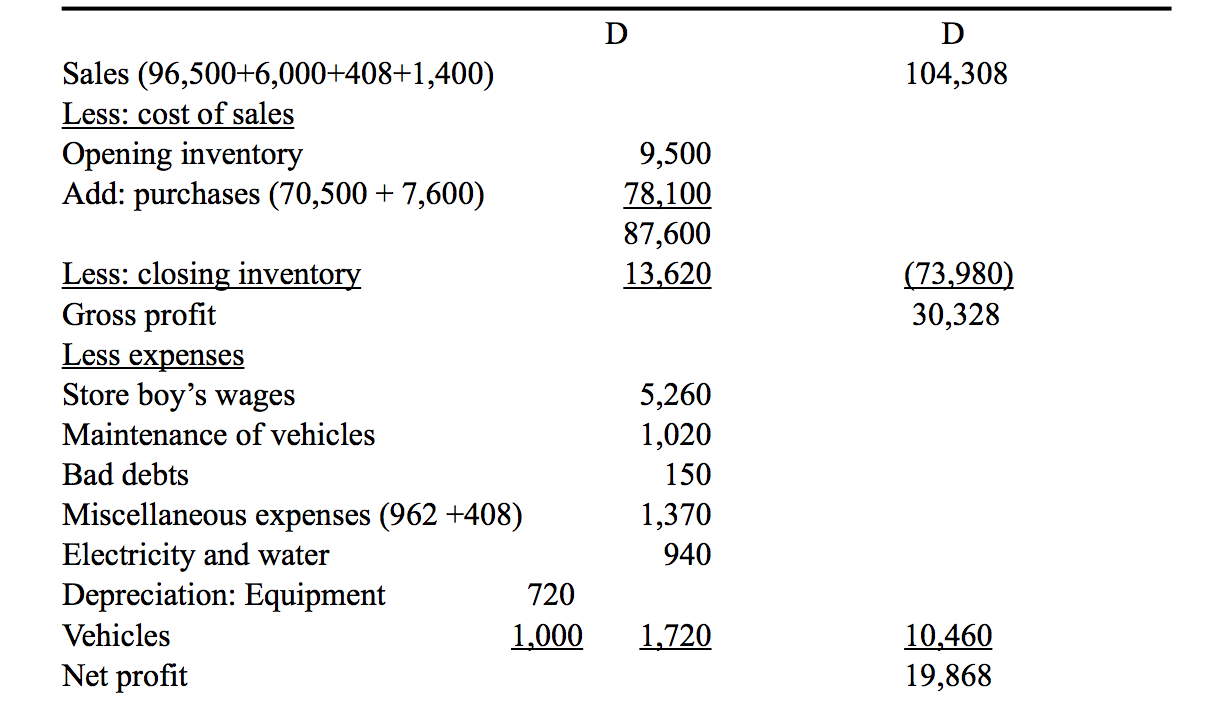

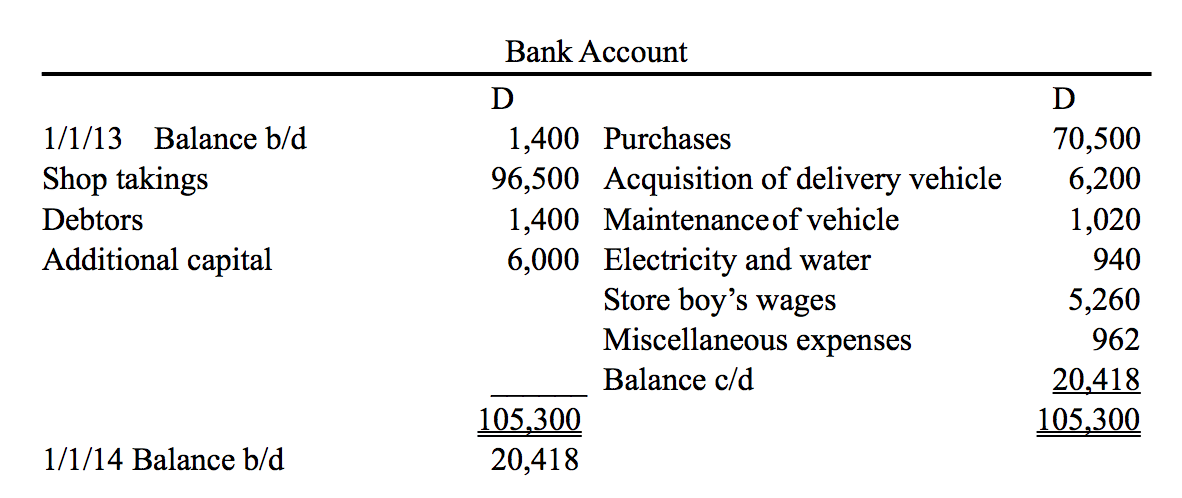

7. Question

Additional information

(i) Dauda paid all shop takings for the year into the bank apart from monthly drawings of D500 and miscellaneous expenses of D408

(ii) He was owing D7,600 to suppliers for inventory bought

(iii) The accounts receivable is t be treated as bad debts

(iv) Inventory was valued at D13,620

(v) Depreciation for the year was calculated as D720 for equipment and D1,000 for vehicles

You are required to prepare

(a) Statement of affairs as at 01/01/13

(b) Income statement for the year ended 31st December 2013

(c) Bank account-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 8 of 9

8. Question

Govu, Tuga, and Kano are partners engaged in retail business, sharing profits and losses in the ratio 2:1:2 respectively. The following are the details of the extracts from their books as at 31st January 2013

Additional information

(i) The firm’s sundry assets were valued at GHc431,000

(ii) The firm was cash strapped and on 01/07/2013 Tuga advanced a loan of GHc100,000 to the partnership at the rate of 5% per annum interest was payable six monthly and was to be credited to his account

(iii) Govu and Kano were to receive salaries of GHc25,000 per annum each

(iv) The profit for the partnership before charging loan interest was GHc158,000 for the year ended 31st December 2013. the loan was not repayable until after the year 2016

You are required to prepare

(a) Profit and loss and appropriation account for the year ended 31st December 2013

(b) Partners’ current accounts in a column form-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 9 of 9

9. Question

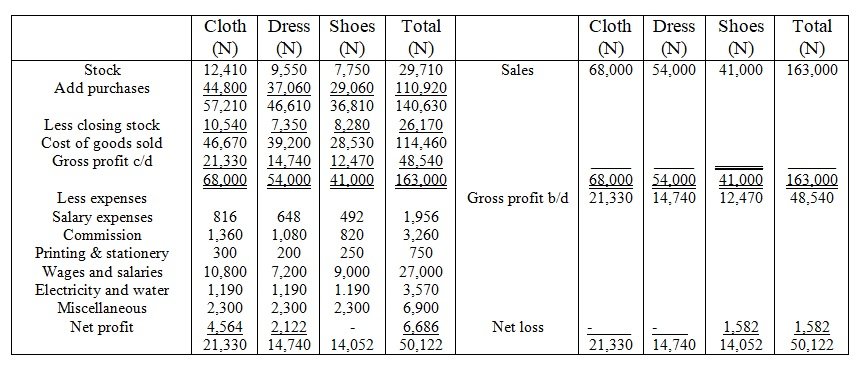

The following balance was extracted from the books of Emeka Company Limited for the year ended 31st December 2016

Additional information

Expenses are to be apportioned between departments as follows

(i) Sales expenses and commission in proportion to sales

(ii) Printing and stationery; wages and salaries in the proportion 6:4:5 respectively

(iii) Other expenses equally

You are required to prepare a departmental trading profit and loss account for the year ended 31st December 2016

-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

Responses