WAEC: FINANCIAL ACCOUNTING

Quizzes

-

2014 Financial Accounting WAEC Objective Past Questions

-

2014 Financial Accounting WAEC Theory Past Questions

-

2015 Financial Accounting WAEC Objective Past Questions

-

2015 Financial Accounting WAEC Theory Past Questions

-

2016 Financial Accounting WAEC Objective Past Questions

-

2016 Financial Accounting WAEC Theory Past Questions

-

2017 Financial Accounting WAEC Theory Past Questions

-

2017 Financial Accounting WAEC Objective Past Questions

-

2018 Financial Accounting WAEC Objective Past Questions

-

2018 Financial Accounting WAEC Theory Past Questions

-

2019 Financial Accounting WAEC Objective Past Questions

-

2019 Financial Accounting WAEC Theory Past Questions

-

2020 Financial Accounting WAEC Objective Past Questions

-

2020 Financial Accounting WAEC Theory Past Questions

-

2021 Financial Accounting WAEC Objective Past Questions

-

2021 Financial Accounting WAEC Theory Past Questions

Quiz Summary

0 of 9 Questions completed

Questions:

Information

You have already completed the quiz before. Hence you can not start it again.

Quiz is loading…

You must sign in or sign up to start the quiz.

You must first complete the following:

Results

Results

0 of 9 Questions answered correctly

Your time:

Time has elapsed

You have reached 0 of 0 point(s), (0)

Earned Point(s): 0 of 0, (0)

0 Essay(s) Pending (Possible Point(s): 0)

Categories

- Not categorized 0%

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- Current

- Review

- Answered

- Correct

- Incorrect

-

Question 1 of 9

1. Question

(a) Outline two differences between bookkeeping and accounting

(b) List one source document used for each of the following transactions:

(i) Sales

(ii) Purchases

(iii) Cash deposit

(iv) Salary(c) State three purposes of source documents

-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 2 of 9

2. Question

(a) What is a not-for-profit making organization?

(b) Outline two differences between not-for-profit making organizations

(c) Explain the following sources of funding in a not-for-profit making organization:

(i) Subscription

(ii) Life membership fee

(iii) Entrance fee

(iv) Donation-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 3 of 9

3. Question

(a) Explain the term fixed capital account

(b) State three conditions that would result in a change in profit and loss sharing ratio of a partnership

(c) Outline three circumstances that would give rise to the creation of goodwill in a partnership

-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 4 of 9

4. Question

(a) List:

(i.) Three books of accounts used in public sector accounting

(ii.) Four users of public sector accounting information(b)State four differences between the private sector accounting and the public sector accounting

-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 5 of 9

5. Question

The following transactions were extracted from the books of Odis Enterprises for the year ended 31st December 2018:

i. Cash received from trade debtors GH¢100,000

ii. Cash paid to suppliers GH¢72,000

iii. Expenses paid during the year were: rent GH¢2,500 general expenses GH¢1,800

iv. A cash of GH¢5,200 was withdrawn by the proprietor for personal use

v. Fixed assets valued at GH¢8,000 on 31st December 2017 were to be depreciated at 10% per annum

Additional Information

You are required to prepare:

(a) Statement of Affairs as at 1st January 2018;

(b) Cashbook:

(c) Trading Profit and Loss for the year ended 31st December 2018-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 6 of 9

6. Question

The books of Omiye Social Club showed the following information for the year ended 31st December, 2015.

You are required to prepare:

(a)Income and Expenditure Account for the year ended 31st December 2015.

(b)Balance sheet as at that day.

-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 7 of 9

7. Question

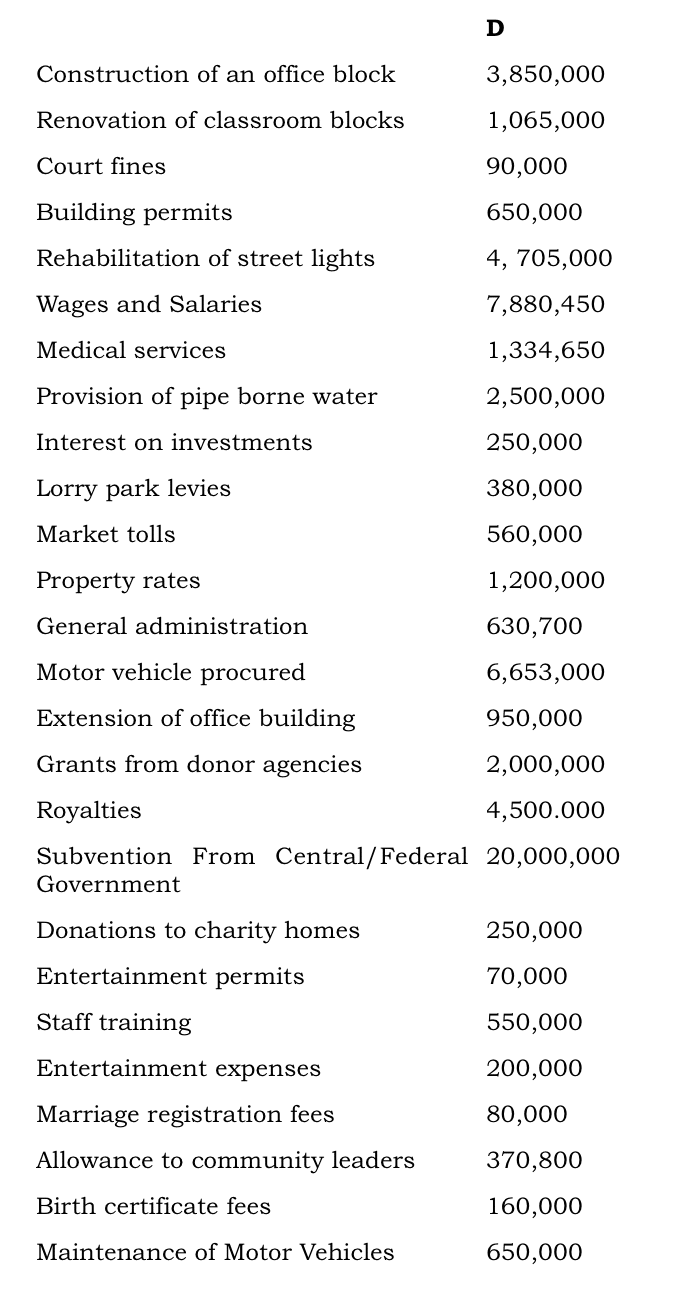

The following balances were extracted from the books of Abobaku Local Government for the year ended 31st December, 2019.

You are required to prepare for the ended 31st December, 2019:

(a) Statement of Recurrent Expenditure

(b) Statement of Capital Expenditure

(c) Statement of Revenue.

-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 8 of 9

8. Question

Yallawa Stores Ltd. has two departments. The following balances were extracted from its books as at 31st December, 2017.

Additional Information:

Expenses are to be apportioned to the department as follows:

i. Commission – on the basis of sales:

ii. Salaries and wages – 3:2 for Department A and B respectively

iii. Discount received – 10% of purchases:

iv. Other expenses are to be apportioned equally.

You are required to prepare a Departmental Trading, Profit, and Loss Account for the year ended 31st December 2017

-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

-

Question 9 of 9

9. Question

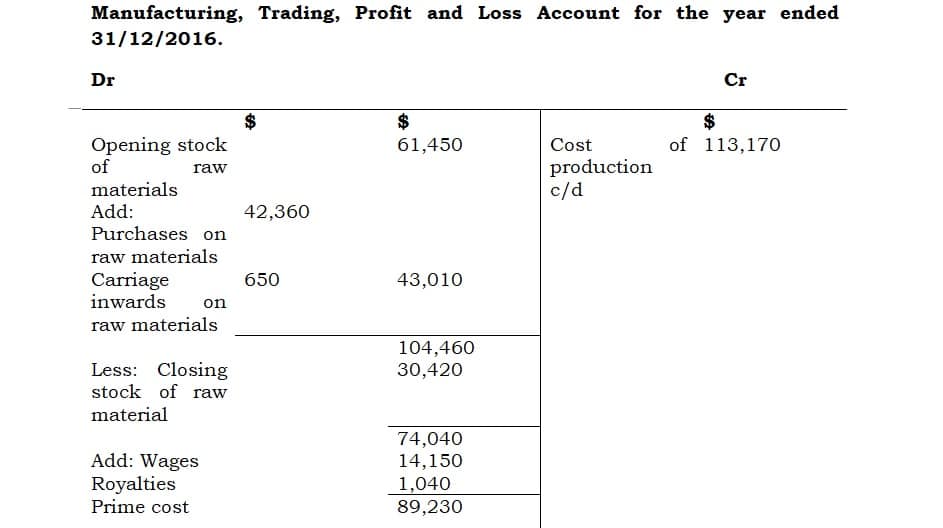

The following information was extracted from the books of Okere Manufacturing Company for the year ended 31st December 2016.

You are required to prepare a Manufacturing, Trading, Profit, and Loss Account for the year ended 31st December 2016.

-

This response will be reviewed and graded after submission.

Grading can be reviewed and adjusted.Grading can be reviewed and adjusted. -

Responses